You're the Biggest Buyer Group in the Country.

So Why Does It Still Feel Impossible?

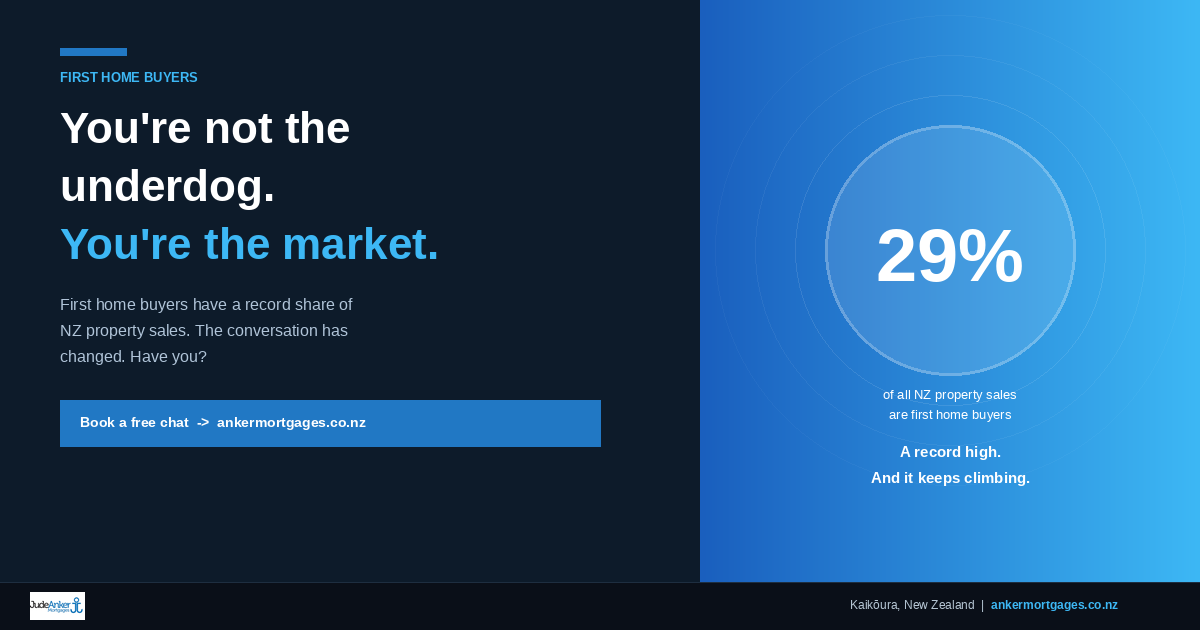

Here's a fact that might surprise you: first home buyers currently make up around 29% of all property purchases in New Zealand. That's a record high. That means roughly one in three homes sold right now is going to someone buying for the very first time.

You are not the underdog. You are the most active buyer group in the entire market.

So why does nobody tell you that? And why does it still feel like the odds are stacked against you?

The Story You've Been Told

The narrative around first home buying in New Zealand has a habit of being exhausting. Rising prices. Deposit hurdles. Tight lending rules. The comparison to what your parents paid for their first home in 1994. It's relentless, and it has a way of making people feel like they missed some imaginary window that closed before they even had a chance to reach it.

What that narrative leaves out is context. The market has shifted. Lending criteria have evolved. The tools available to first home buyers today are meaningfully different from what existed even five years ago, and most people either don't know about them or don't have anyone in their corner who can explain how they actually work.

That gap between what's possible and what people believe is possible is exactly where deals fall apart before they even start.

What's Actually Working in Your Favour

Your deposit may not need to be 20%.

The standard deposit benchmark gets repeated so often that most people assume it's a legal requirement. It isn't. Lending policies vary by lender, and a well-presented application to the right bank can unlock significantly lower deposit requirements for eligible first home buyers. The key word there is well-presented. A lender who sees a clean, consistent picture of your income, spending, and savings history reads an application very differently from one that's been submitted cold with gaps and unexplained transactions.

KiwiSaver is doing more work than most people realise.

If you've been in KiwiSaver for three or more years, your contributions can go toward your deposit. This is not a bonus or a loophole. It's how the scheme was designed. The numbers can be significant, particularly for buyers who have been contributing for several years without ever stopping to calculate what they've actually accumulated.

The Kainga Ora First Home Loan exists specifically for you.

With eligible lenders and a qualifying income, this government-backed scheme lets first home buyers purchase with as little as a 5% deposit. It has income caps and regional price caps, so it doesn't suit everyone, but for buyers who fit the criteria, it removes one of the most frequently cited blockers entirely.

Regional New Zealand is a genuine opportunity, not a consolation prize.

The conversation about property affordability tends to be dominated by Auckland and Wellington. That framing ignores the fact that there are excellent, liveable communities across New Zealand where property is priced within reach of first home buyers, and where the lifestyle return on that investment is hard to beat.

Kaikōura is one of those places. After a post-earthquake correction reset values and a Covid-era spike unwound, prices have stabilised into a market that gives buyers time to make good decisions rather than panicked ones. For anyone open to a lifestyle shift, regional centres deserve serious consideration rather than being dismissed as a fallback.

The Part Nobody Talks About: How You Present Matters

Banks are not in the business of telling you why you couldn't borrow. They assess what's in front of them and make a decision. If the picture they see is incomplete, inconsistent, or presented in a way that raises questions, the answer is no. It's not personal. It's procedural.

A good mortgage adviser's job is to build that picture before it ever reaches a lender, and to know which lenders read which profiles most favourably. That means understanding your income structure, your spending patterns, your savings history, and what each institution is likely to weight more or less heavily right now.

That's not a small thing. It's the difference between an approval and a decline on a customer who shouldn't have been declined.

The 29% Isn't an Accident

First home buyers aren't at a record share of the market because they got lucky. They're there because a lot of them got prepared, got good advice, and got moving. The ones who are succeeding aren't necessarily the ones with the biggest salaries or the longest savings history. They're the ones who stopped assuming the answer was no and started asking the right questions of the right people.

If you're a first home buyer trying to work out whether you're closer than you think, that's exactly the conversation we're here to have.

Talk to the team at Jude Anker Mortgages.

We're based in Kaikōura and we work with buyers across New Zealand. No obligation, no jargon, just a straight conversation about where you actually stand.

Email: support@ankermortgages.co.nz