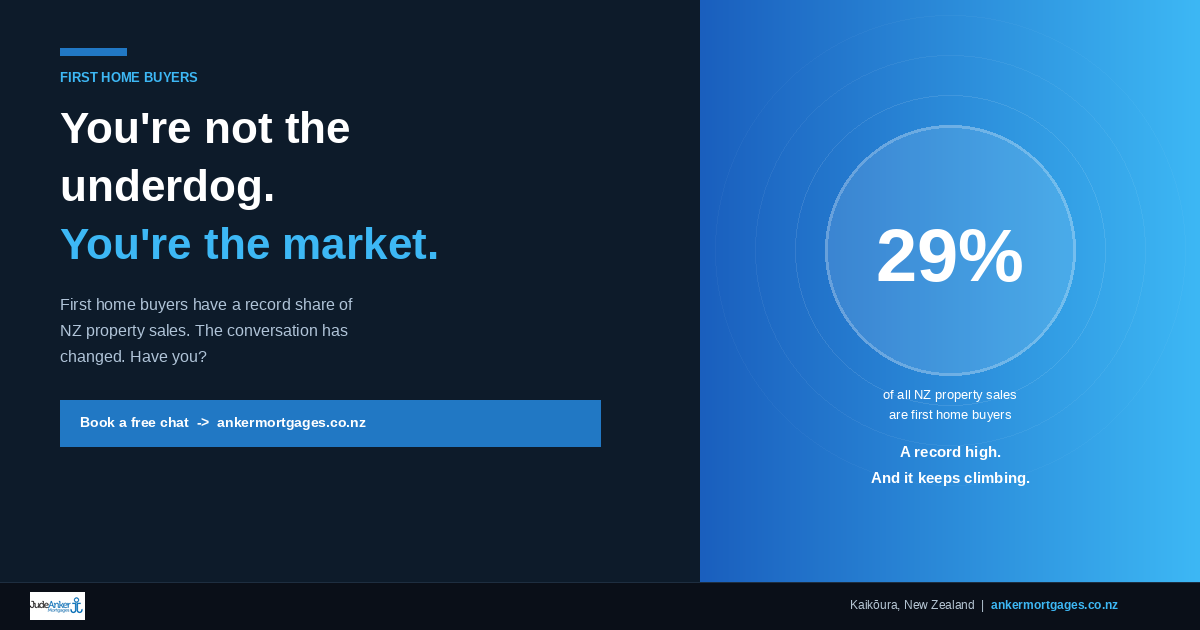

You can't live there - but you can still buy your first home

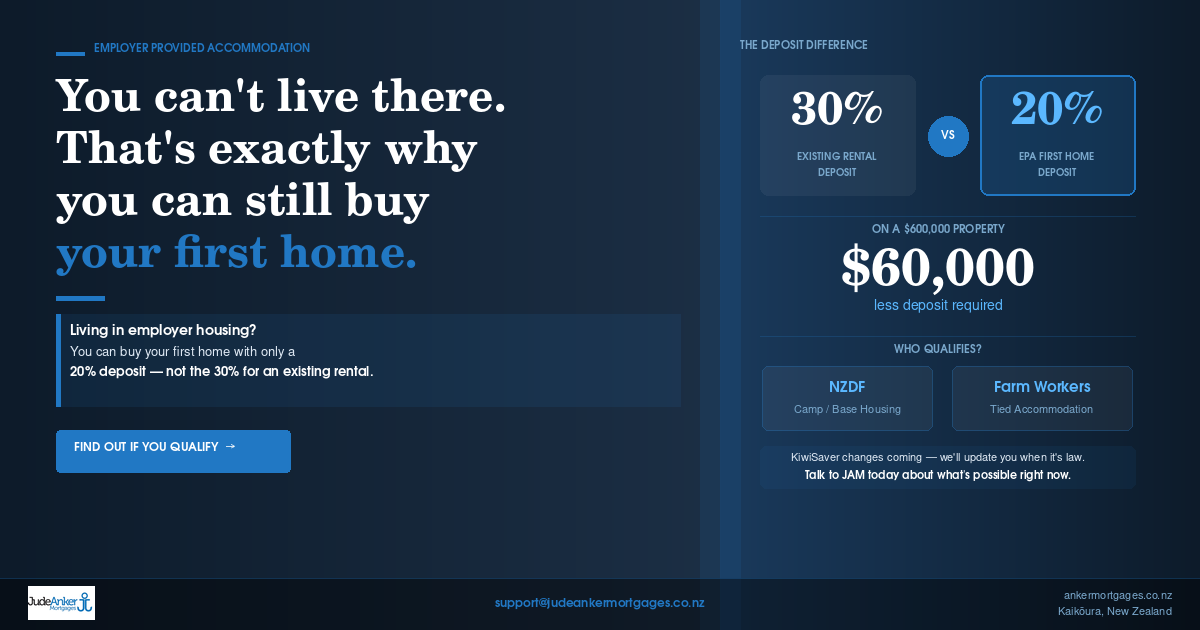

Living in employer housing?

If you're NZDF or working in tied farm accommodation, here's something most people in your situation don't know: you can still buy your first home while living in employer-provided housing — and you only need a 20% deposit, not the 30% required for an existing rental property.

The policy is called Employer Provided Accommodation. It exists specifically because some people have no choice about where they live. Camp housing, base housing, a farm cottage, an on-site worker's dwelling — if your job comes with your accommodation, certain lenders will still treat your purchase as a first home, not an investment property. That single distinction saves you 10% of the purchase price in deposit. On a $600,000 property, that's $60,000.

Here's how it works: you buy the property, tenants move in and cover the mortgage while you remain in your employer-provided housing, and the home becomes yours to live in when your circumstances change — when the posting ends, when the farm job moves on, when the time is right.

You'll need a letter confirming your employment accommodation requirement (from your CO if you're NZDF, or your employer if you're in rural work), your last three pay slips, and a declaration that you don't currently own any residential property. That's it.

Most people assume the answer is no before they've even asked the question. Don't be one of them.

Talk to JAM. We work with NZDF Pers and rural clients regularly and we know exactly how to make this work.